The Small Business Health Insurance Tax Credit

Jun 9th, 2014

Credit: Kenny Louie via Flickr under Creative Commons

New York State’s small businesses are in for a big year in 2015. Next year the Affordable Care Act’s (ACA) employer mandate for small businesses employing 50 or more full-time workers goes into effect. And if you do meet the small business mandate then your business may qualify for the small business health insurance tax credit. However, for the mandate, a full-time employee, or FTE, is considered to be any person, excluding the owner, who works at least 30 hours each week.

The mandate is also a bit tricky in that the hours worked by part-time employees are added together and divided by a 30-hour work week. Meaning that two part-time employees would be equivalent, in the eyes of the ACA, to one FTE.

So if the employer mandate is only for those businesses with 50 or more FTEs then is there any incentive for businesses with fewer employees to offer health insurance? In fact, businesses with 25 or fewer FTEs who offer a health insurance option can potentially receive a sizable tax credit towards the cost of such coverage.

The small business health insurance tax credit

This small business health insurance tax credit has been in effect since the ACA was signed into law. As a business owner if you offered coverage, but did not know about the credit you can still file for it for the previous years. Let’s take a look at the specifics of the tax credit, and see how your business might benefit.

The major benefit of the small business health insurance tax credit is of course the financial aspect. It can potentially reimburse you for up to 50 percent of the cost of providing your workers with health insurance. However, to qualify for the credit there are a few requirements to meet.

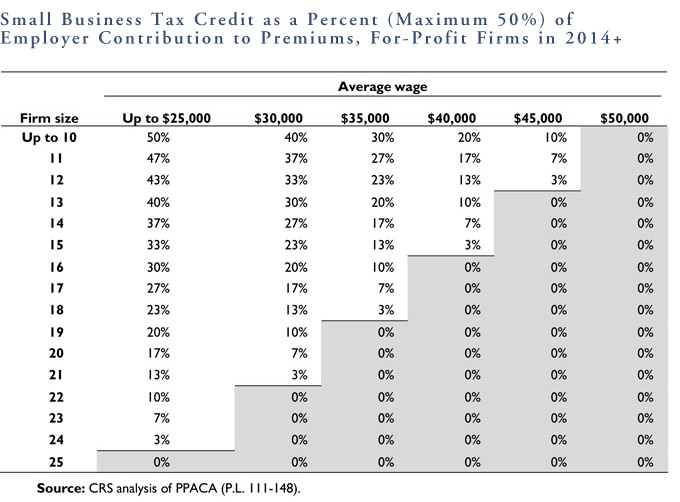

First, you must have 25 or fewer FTEs, working at your company excluding the owner. The average annual salary of these FTEs should be $50,000 or less, and the business must contribute at least 50 percent of the lowest cost employee coverage premium that is offered.

The maximum tax credit of 50 percent of health insurance costs goes to businesses with 10 or fewer FTEs. But even those businesses with more than 10 and less than 25 FTEs can still receive substantial savings through the credit. Essentially the more FTEs a business has and the more they are paid, the smaller the tax credit will be.

The chart below, courtesy of the New York State Health Insurance Exchange, breaks down the possible small business tax credit amounts in New York State. It should also be noted though that for your business to receive the health insurance tax credit for 2014, you need to have purchased your small business health insurance plan through the New York State of Health Insurance Exchange’s Small Business Health Insurance Options Program, or SHOP.

The SHOP exchange in New York State is very similar to the individual health insurance exchange at HealthCare.gov. At the New York SHOP Exchange, you’re able to look for health insurance by price, carrier, and/or region, except that the plans are geared towards small businesses, rather than individuals.

Because of this stipulation of the tax credit, if you are grandfathering in your older small group plan for your business, then you will not be eligible for the small business health insurance tax credit when you file your 2014 taxes.

The upside of employee health insurance

Small businesses are without a doubt the backbone of New York State’s economy, especially those businesses that are small enough to fall outside of the ACA’s employer mandate. Those smaller businesses are accounting for some of the strongest job growth in the state. With so many people finding new jobs in this area of the economy, what are they going to do about health insurance?

For many owners, the idea of adding yet another thing to the seemingly unending list of expenses and regulations that small businesses need to deal with may sound like too much of a burden. It may sound downright crazy. Especially because if you employ fewer than 50 FTEs, you don’t need to worry about the employer mandate at all.

However, there is an argument to be made for the correlation between long-term business growth and offering your employees health insurance. The extra value of offering health insurance will no doubt increase retention rates, especially among the more senior and experienced employees. Not to mention having a benefits package that includes health insurance can improve company morale.

Of course, there is also the obvious benefit of the increased productivity that comes with having a healthy workforce. Your employees will be able to see a doctor before their health problems become so serious they need to miss weeks of work. Just think how much more productive flu season could be for you if no one had to miss a day of work.

While the tax credit is a powerful incentive for some businesses to offer health insurance, it won’t be possible for everyone to take advantage of it. Luckily for people working at those companies, they can still purchase a reasonably priced individual health insurance plan, perhaps with a subsidy, at the New York State Health Insurance Exchange.