Shop Affordable 2020 New York PPO Plans in all 62 Counties

Are you shopping for a New York PPO plan? Are you looking to better understand the New York PPO health insurance market and compare NY PPO rates? Here you will find key resources needed to help you make an informed decision on selecting the right New York PPO plan

Are you shopping for a New York PPO plan? Are you looking to better understand the New York PPO health insurance market and compare NY PPO rates? Here you will find key resources needed to help you make an informed decision on selecting the right New York PPO plan

TABLE OF CONTENTS

-

New York PPO Insurance Carriers

-

What to Know When Shopping for a New York PPO Insurance Plan

-

New York PPO Rates for 2020

-

Essential Health Benefits

-

Most Common Questions Regarding A New York PPO Health Plan

New York PPO Insurance Carriers

New York PPO Insurance Carriers

Below is the list of carriers that currently offer New York PPO health insurance plans for sale in 2020 for Small Businesses. Only select carriers have plans available to working individuals, Freelancers, and the self-employed. Please call for the latest carrier information.

- Aetna

- Cigna

- EmblemHealth

- Empire (BlueCross BlueShield)

- Health Insurance Plan of Greater New York (HIP)

- HealthNow (BlueCross BlueShield)

- MVP Health Care (Mohawk Valley Physicians Health Plan)

- Oxford

- United Healthcare of New York

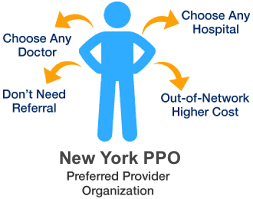

What to Know When Shopping for a New York PPO Insurance Plan

What to Know When Shopping for a New York PPO Insurance Plan

Below are some of the most common concerns when shopping for a New York PPO health insurance plan.

Are Your Doctors In-Network – Before purchasing a health insurance plan you should always make sure that your doctor(s) are part of the network even though a NY PPO plan will cover out-of-network services. Going to an out-of-network doctor may cost substantially more than if that doctor is in-network.

Don’t just ask the doctor’s office if they accept a certain insurance plan before you enroll. You should always confirm with the insurance company or an agent that your doctors are in-network. Why the concern? Well, keep in mind that if an out-of-network provider suggests services, then all of those services provided by that recommended doctor will be considered out of network, even if the facilities and providers are in-network. With a NY PPO health plan, any of your out-of-network medical services will go towards your out-of-network deductible

Lower Monthly Premium May Result in Higher Costs– Health insurance follows a simple formula: the lower your monthly premium is, the more likely you are to pay higher costs when you use the insurance. If you’re someone who happens to be in good health and does not foresee any health-related issues and doesn’t use medicine on a very regular basis, then perhaps you’re better off opting for a lower costing health insurance plan. However, if you find that your medical expenses and prescription usages are high, then you may save money by purchasing a plan that costs more per month. Be sure to consider your current health condition when shopping for a New York PPO health insurance plan.

Health Insurance is a Contract – When purchasing a NY PPO health plan, both parties agree to live up to the contract (usually for one year). If you find that you are not happy with your plan, you can’t go back to your insurance company mid-year and ask them to change coverage. As such, be sure to choose the right plan that suits your needs before signing the contract. If you find that you have had a State Marketplace plan that has lapsed, you’re able to get a NY PPO health plan mid-year as long as you are employed.

Types of Insurance Coverage – EPO, PPO, POS, HMO, HDHP, and HSA. The first 4 are acronyms that describe different types of health insurance coverage, which provide you with or without the flexibility to see specialists and receive out-of-network and out-of-state care. Also, different plans have different requirements related to the need for referrals. If you’re often seeing specialists out-of-network then you want a plan that offers that flexibility.

If you find that you travel often for work or live in multiple states per year, then perhaps a New York PPO plan that offers that flexibility is needed. The last two types, HDHP and HSA’s allow you to set up a tax-free savings account specifically for qualified medical costs For a better understanding of these types of coverage please refer to the following article.

Are Essential Health Benefits Covered? – All New York PPO plans cover the 10 essential health benefits. This provides you with a guaranteed minimum level of coverage, which is the standard set by the Affordable Care Act. Why would we need a minimum standard level? Well, the cost of medical care is prohibitive without insurance in place and can often lead to financial ruin. Ensuring that a plan includes the minimum essential health benefits provides a safeguard.

Premium, Deductible, and Out-Of-Pocket Costs. Each term relates to the cost of using and maintaining your plan.

- Premium is the cost of the insurance that you usually pay monthly to the insurance company. Premiums are often locked in for one year, meaning the insurance carrier cannot arbitrarily charge you a higher premium within that year

- A deductible is a yearly dollar threshold that you must meet before the insurance company paying for medical services. This almost always excludes preventative care. With a New York PPO health plan, there is a separate out-of-network deductible that must be met before any out-of-network services are covered

- Out-of-pocket costs are the maximum annual dollar amount that you can spend on health care services and medicine. There are separate out-of-pocket maximums for in-network services and out-of-network services

New York PPO Rates for 2020

New York PPO Rates for 2020

Below is a table of Individual New York PPO plans. The information below such as Rates and benefits are approximated. Please call for specific plan information

| Benefits | In-Network | Out-of-Network | Age 19 – 64 | |

|

NY PPO 1

|

Office Copay | $20/$60 |

Call for benefits

|

$600+

|

| Deductible | $5,000 | |||

| Maximum OOP | $8,160 | |||

| Rx | 0/25%/50% | |||

|

NY PPO 2

|

Office Copay | $40/$60 |

Call for benefits

|

$750+

|

| Deductible | $4,000 | |||

| Maximum OOP | $8,150 | |||

| Rx | 0/25%/50% | |||

|

NY PPO 3

|

Office Copay | $30/$50 |

Call for benefits

|

$1,100+

|

| Deductible | $1,000 | |||

| Maximum OOP | $8,150 | |||

| Rx | 0/25%/50% | |||

|

NY PPO 4

|

Office Copay | Deductible |

Call for benefits

|

$600+

|

| Deductible | $6,750 | |||

| Maximum OOP | $6,750 | |||

| Rx | Deductible | |||

|

NY PPO 5

|

Office Copay | $40/$60 |

Call for benefits

|

$750+

|

| Deductible | $2,500 | |||

| Maximum OOP | $8,150 | |||

| Rx | 0/25%/50% | |||

|

NY PPO 6

|

Office Copay | $25/$30 |

Call for benefits

|

$900+

|

| Deductible | $350 | |||

| Maximum OOP | $700 | |||

| Rx | 0/25%/50% |

![]()

Essential Health Benefits

What Are Essential Health Benefits? Essential Health Benefits are a set of 10 health care benefits established by the federal government under the Affordable Care Act of 2014. The purpose is to ensure that all persons are covered by a set of minimum standards. Specific insurance services may vary by state and all plans must provide dental coverage for children.

1.Ambulatory Patient Services – Medical care provided without admission to a hospital, including doctor’s office visits, clinics, and outpatient surgery centers.

2.Emergency Services – Organizations that are responsible to deal with emergencies when they occur. This includes medical care that if not treated could lead to serious conditions or disabilities.

3.Hospitalization – Medical care that patients receive when they are hospitalized. This includes the care of nurses, doctors, and other staff. This also includes medication received, room and board, tests, and laboratory work.

4.Maternity – Medical care that a woman receives during pregnancy and post-pregnancy. This includes labor, delivery, post-delivery, and care for newborn babies.

5.Mental Health Services and Addiction Treatment – Patient care provided to evaluate, diagnose, and treat any mental health conditions or substance abuse disorders.

6. Rehabilitative Services and Devices – Services provided after an injury, accident, disability, or a chronic condition. The purpose is to attempt to help regain the patient’s mental and/or physical skills that were lost (to make the person whole again).

7. Pediatric Services – Medical care that is provided to children and infants, including regular check-ups, recommended vaccines, dental, and vision care.

8. Prescription Drugs – Medicine that is prescribed by a doctor, and nurse practitioner, to treat any illness or existing condition.

9.Preventative and Wellness Services and Chronic Disease Treatment – Physicals, Immunizations, and cancer screenings to prevent or detect certain medical conditions, and to provide care for chronic conditions.

10.Laboratory Services – Medical tests that are usually ordered by your doctor which include coverage for X-Rays and diagnostic imaging, blood and fluid tests, biopsies, pathology, and pregnancy tests.

Most Common Questions Regarding A New York PPO Health Plan

Most Common Questions Regarding A New York PPO Health Plan

How much does a New York PPO cost?

New York PPO Health plans are typically more expensive than other plans due to the flexibility that a PPO provides. Use the table above to see NY PPO rates and shop plans in your state

Does my doctor accept New York PPO Insurance?

Locate the list of health insurance companies above and select your company. Once in their network listing, visit the PPO network section. You can always call your doctor’s office, however, it is best to verify with the health insurance company

Where can I buy a New York PPO health insurance plan?

NY PPO Health plans are purchased through NY health insurance broker representatives who can not only set the health plan up but also assist with any premium or claims issues throughout the plan year. It is best to work with a broker that is appointed with every carrier in the area so there is a choice when selecting a carrier and/or plan.

How do I qualify for a NY PPO plan?

To qualify for an NY PPO plan, the person applying must either be employed, self-employed, or a freelancer.

Can I buy a NY PPO plan anytime?

Yes. NY PPO health plans are available to go effective at the beginning of any month during the year. Typically, the application should be complete by the 15th of the prior month for coverage to begin on the 1st of the following month.

What happens if I’m not happy with my NY PPO health plan, can I change it?

Since the PPO plan application is a contract, you cannot change your plan until your PPO plan renews, usually one year after the start date. You can switch NY PPO plans mid-year as long as you change to a different insurance company.

What makes a PPO plan special?

The flexibility of a PPO health plan is what makes it special You can go to any doctor you choose. That’s a great advantage as compared to an EPO or HMO plan where you must use their in-network providers. This is especially true for those who travel often and want to be able to see a doctor or specialist anywhere in the country.

Do I have to be self-employed or part of a group to buy a PPO plan?

There are two ways of getting a NY PPO health plan. As an employee of a company whose company plan is a PPO. The second way is for individuals, freelancers, and sole proprietors to become part of an association that is offering a PPO.

Do the State Exchange and healthcare.gov sell PPO health plans?

For Individual health coverage, no they do not. Only EPO and HMO plans are offered through the Federal Exchange and State Exchanges. For a small business, yes however they are limited.

Do freelancers qualify for NY PPO plans?

A freelancer is considered an individual which therefore means they must join an association that is offering a New York PPO health plan to be eligible for the insurance.

Can I qualify for a PPO plan if I am 65 or older?

Employees of a company that is 65 or older have the option of keeping their NY PPO health insurance plan instead of going on Medicare. If a person is not working for a company, they would not be eligible for a New York PPO plan.

Are PPO plans offered as short-term medical plans?

Yes. If an individual is seeking a short-term medical plan, there are PPO Plans available however many short-term medical plans are not comprehensive health insurance plans so be sure to review the summary of benefits.

Why are PPO plans more expensive than other types of health plans like HMOs?

Due to the flexibility that New York PPO plans offer and higher reimbursement to select doctors and hospitals, they are typically more expensive than an HMO plan where someone must utilize the contracted providers. There is a cost to having the ability to see any provider in the nation.

Why are there more hospitals and doctors in a PPO plan than in non-PPO plans?

Insurance companies pay exclusive doctors and hospitals above-average reimbursement rates to have them participate in New York PPO plans. As such those doctors who don’t accept the reimbursement rate of lesser plans such as HMOs will often participate in a PPO.